Overview

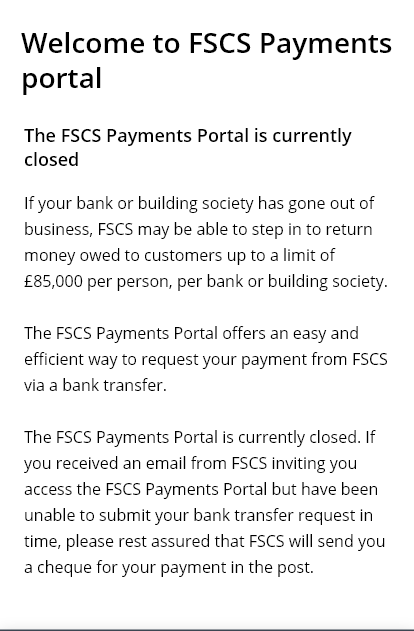

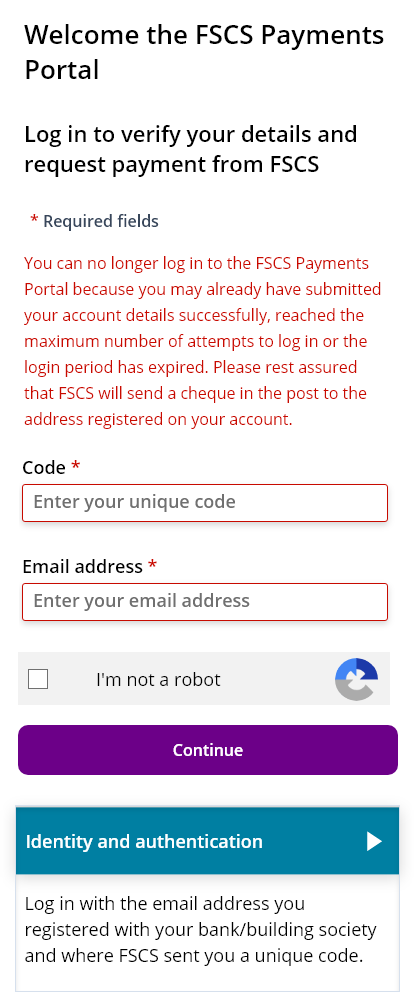

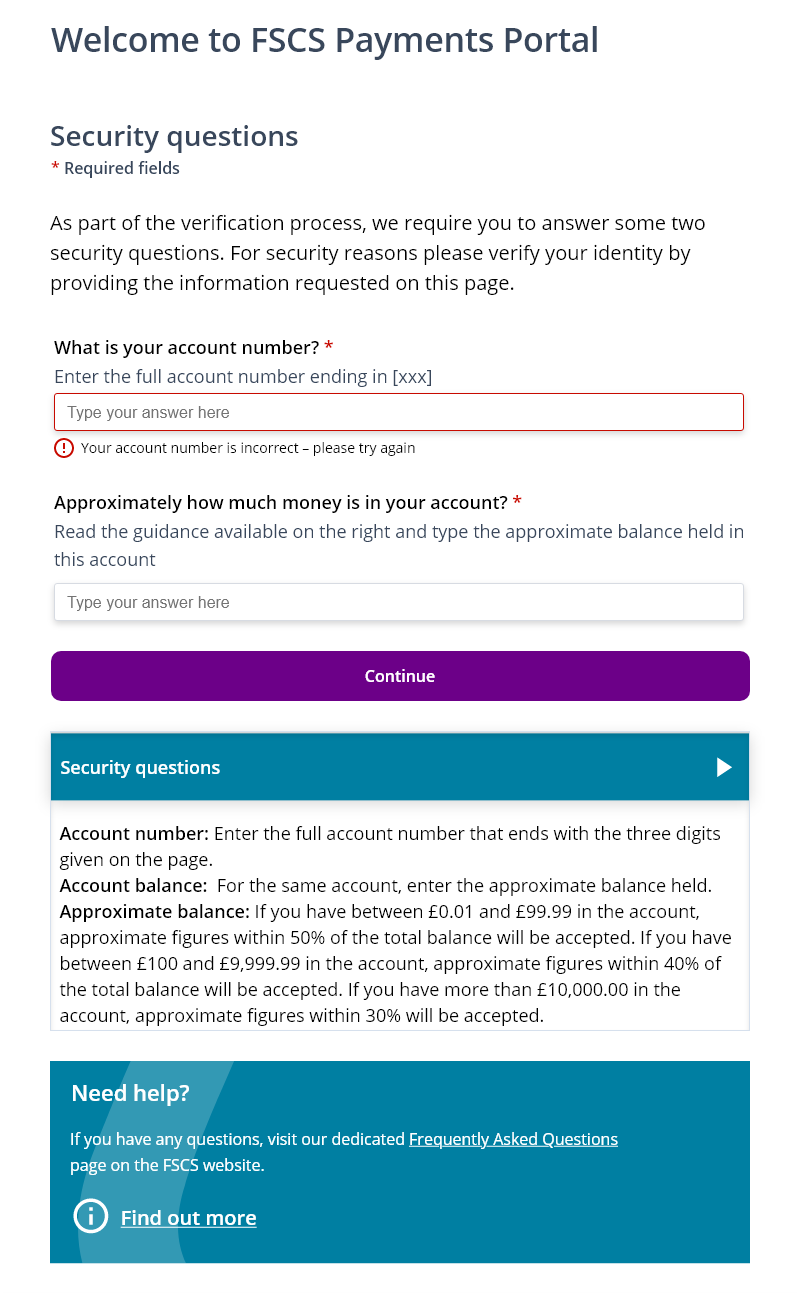

End-to-end delivery of a newly mandated regulatory solution, enabling customers to reclaim funds from failed deposits through a secure self-service portal.

Expetise applied

User experience User | interface design | research | content design | email marketing product design & innovation | problem solving | stakeholder management

Requirement

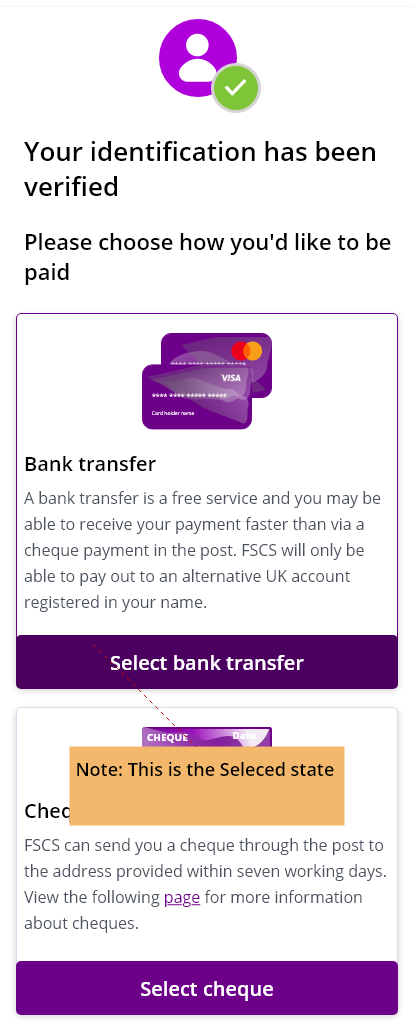

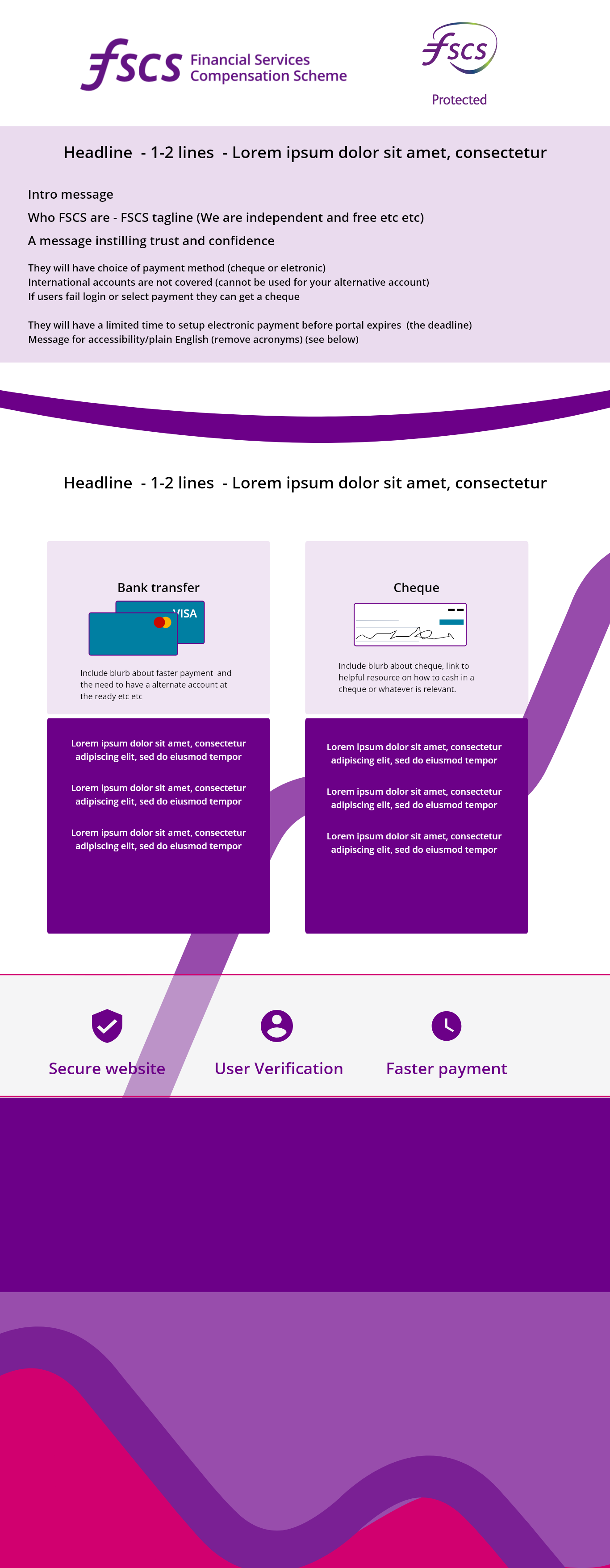

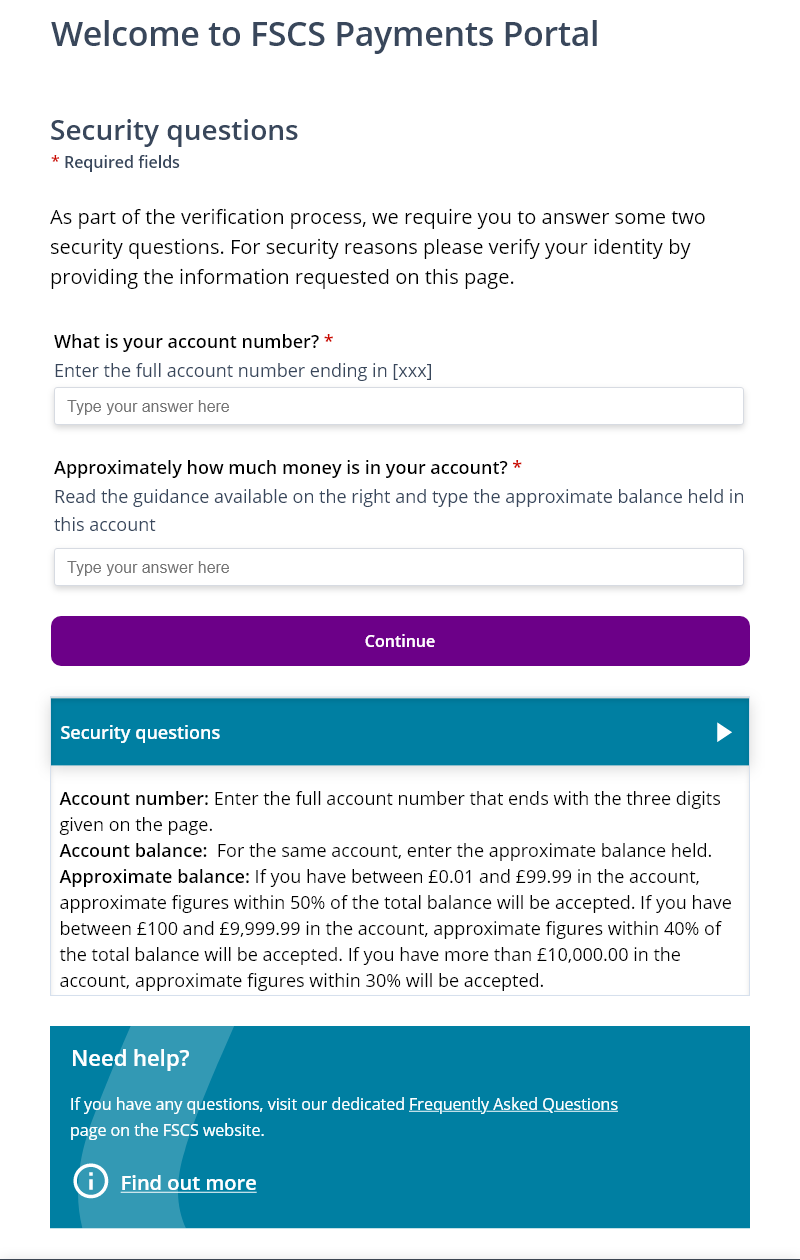

Develop an interim digital portal accessible to depositors with registered email addresses, with Faster Payments functionality as the preferred method for compensation delivery.

Background

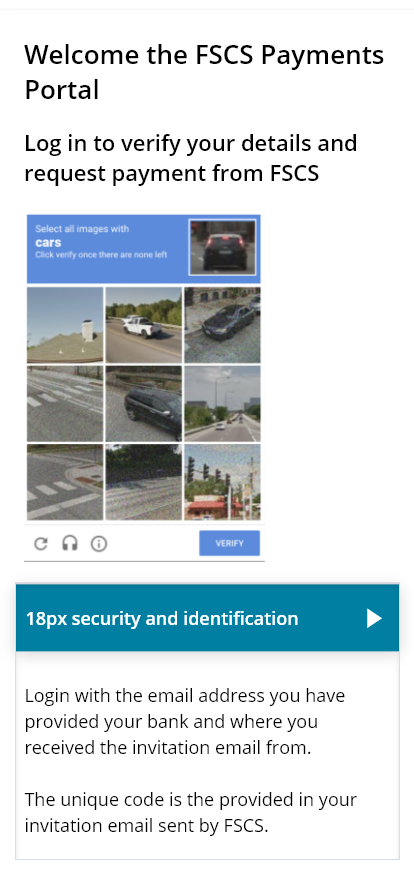

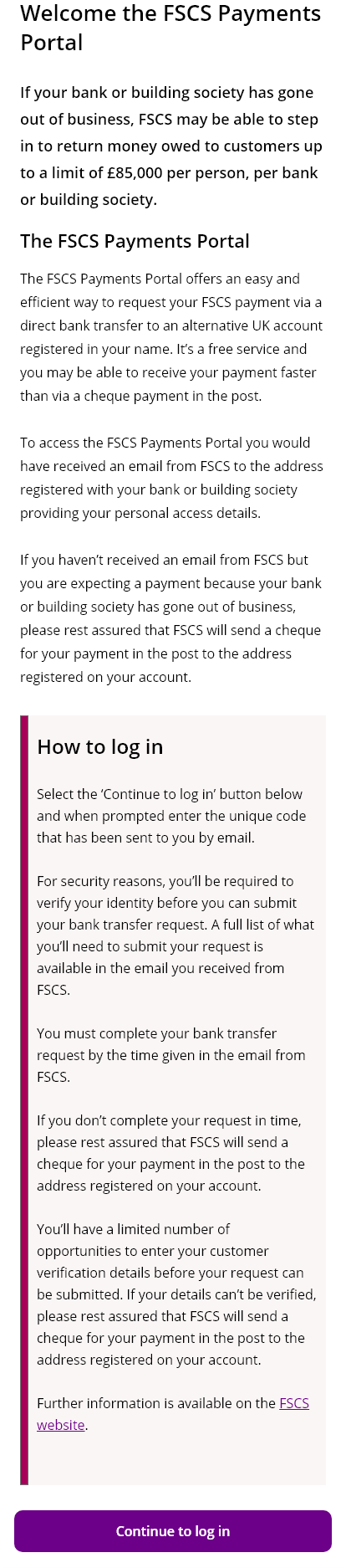

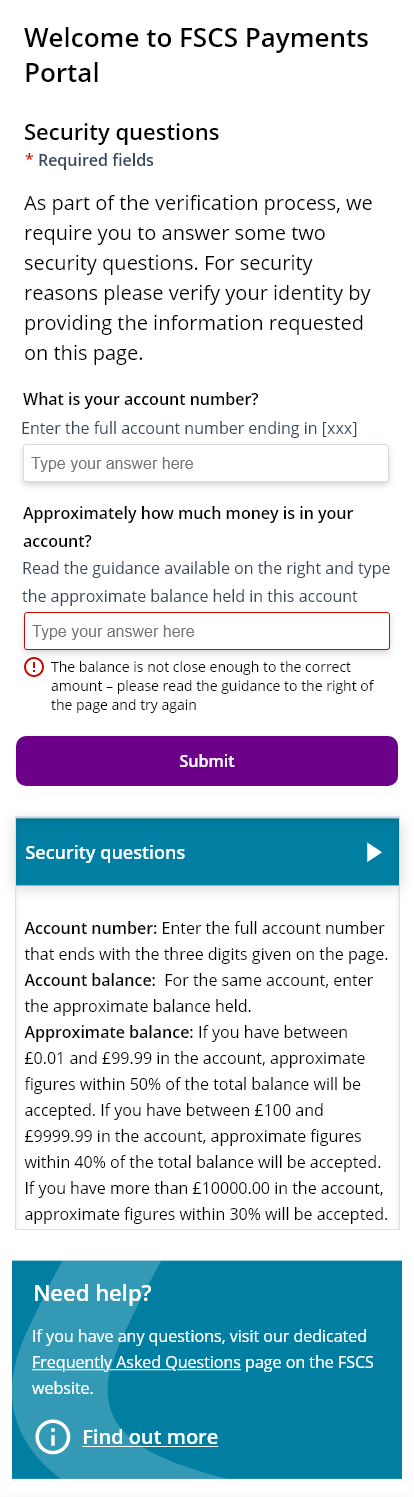

Regulation requires FSCS to provide depositors with a secure, digital option to review compensation details and receive payments electronically.

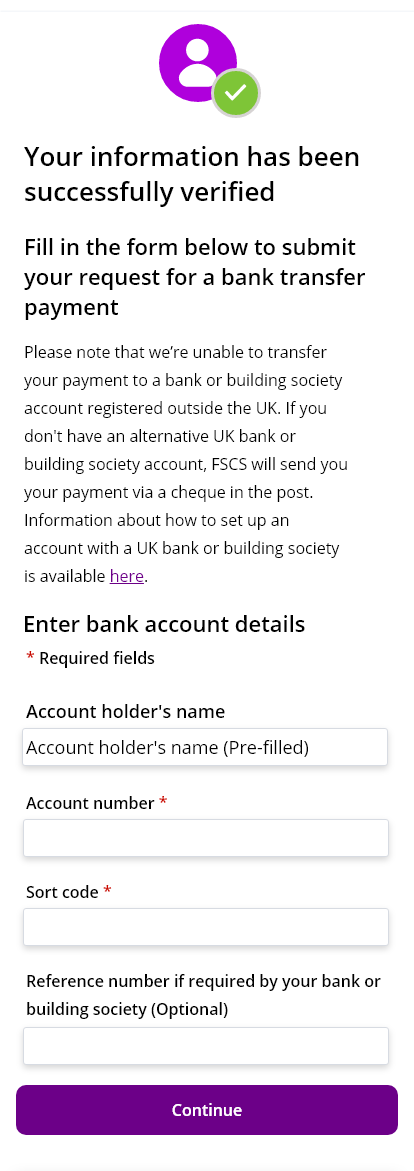

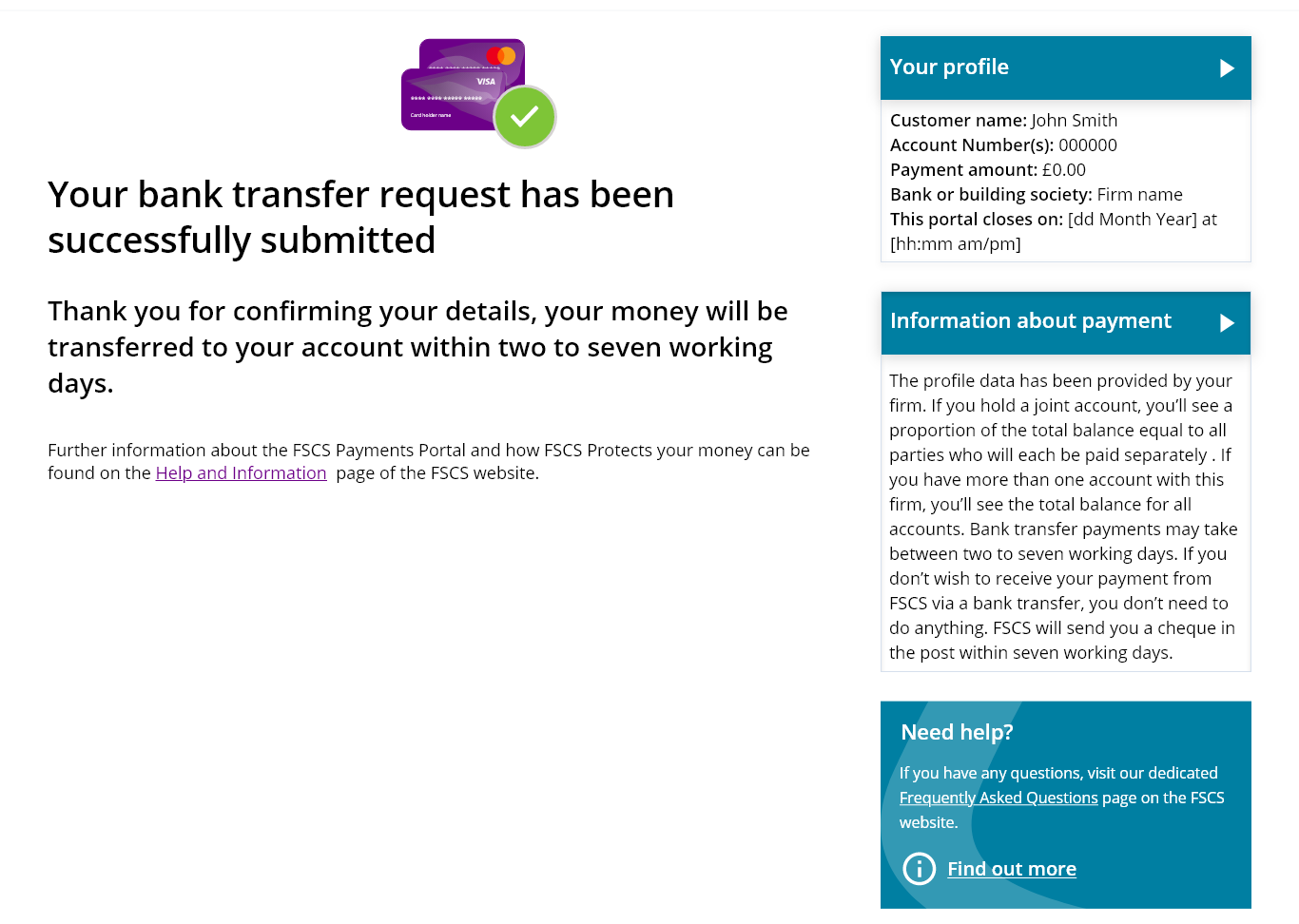

- Depositors with email addresses are invited to a secure FSCS portal to review their compensation and receive funds via Faster Payments.

- Depositors without email access continue to receive compensation via the existing postal cheque process.

- This ensures no depositor experiences a worse compensation journey than the current baseline.

Objective

For depositors with valid SCV email addresses, the interim solution aims to:

Delivering a new, regulator-mandated solution within tight timelines

Balancing security, trust, and usability for users unfamiliar with FSCS interactions

Designing a system capable of handling sensitive financial data securely

Adapting to evolving requirements and stakeholder inputs

Leveraging existing third-party capabilities while enhancing internal technical capacity

For those unable to access the portal:

compensation defaults to cheque distribution, ensuring equitable service.

Additionally, all depositors are supported with guidance on accessing services such as Current Account Switching and Basic Bank Account setup.

Challenges

Delivering a new, regulator-mandated solution within tight timelines

Balancing security, trust, and usability for users unfamiliar with FSCS interactions

Designing a system capable of handling sensitive financial data securely

Adapting to evolving requirements and stakeholder inputs

Leveraging existing third-party capabilities while enhancing internal technical capacity

To mitigate risk, the approach prioritised:

Use of off-the-shelf capabilities through FSCS technical partners

Incremental enhancement of in-house systems

Minimising delivery complexity while ensuring operational reliability

Delivery Approach

Phased rollout:

- Core functionality was delivered iteratively across multiple phases

- This allowed improvements to be released rapidly while reducing delivery and operational risk

Interim solution focus:

Immediate emphasis was placed on designing and delivering a viable solution within the 2023/24 timeframe

A roadmap was established to guide future enhancements and expansion of functionality

Design Process

As the sole designer, I led the end-to-end design under a six-month delivery timeline, navigating evolving requirements and high complexity.

- Key considerations included:

- Security and user trust

- Data handling and system integration

- Communication clarity for first-time FSCS users

- Cross-functional alignment across business, engineering, communications, and deposit teams

- My role extended beyond UX/UI design to include:

- User research and testing

- UX writing and content strategy (emails, portal, and web)

- Translating complex requirements into a coherent, user-friendly system

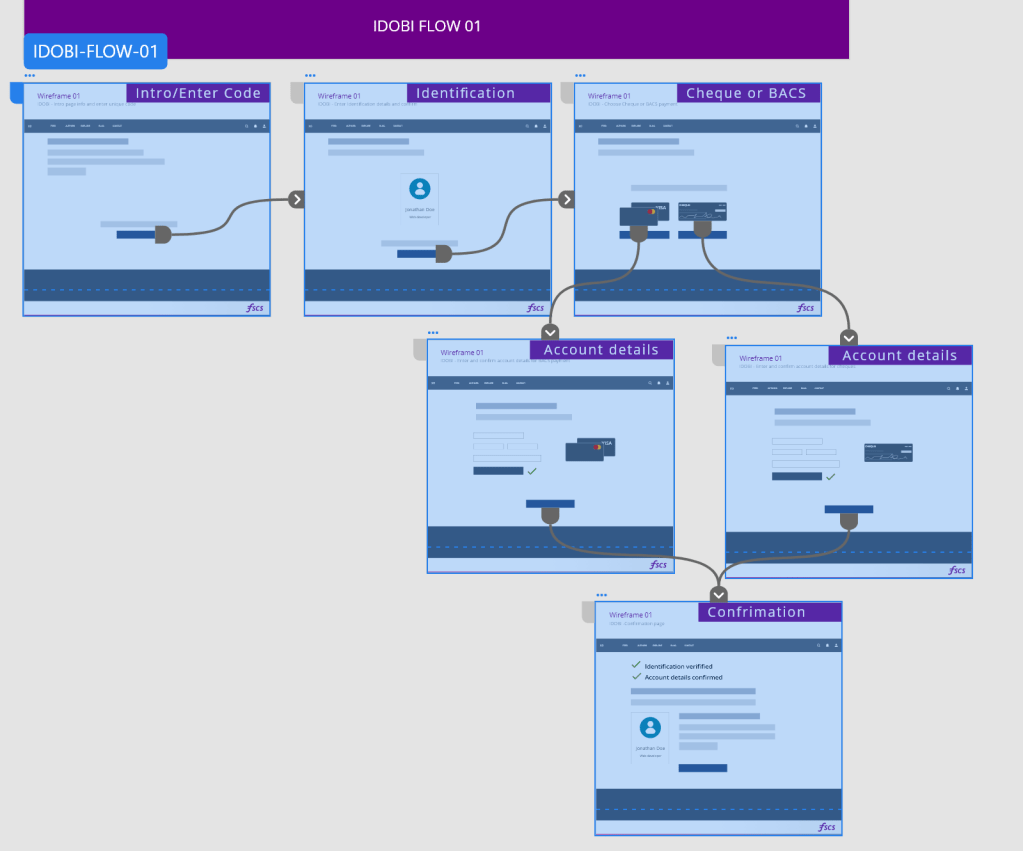

Design stages included:

- UX/UI refinement and functional definition

- Wireframing and conceptual prototyping for stakeholder alignment

- High-fidelity design development across multiple iterations

- Creation of evolving design systems/styles as requirements changed

- Final UI designs with guided (“dummy”) content

- Email template design and supporting communication flows

- UX-led copywriting and content proofreading

Outcomes

- The portal was successfully deployed and operational within two months of launch

- It efficiently processed customer claims following deposit failures

- The solution has since become an integral part of FSCS’s response to deposit failures

Future considerations:

- Further development is required to support Credit Union failures, currently constrained by regulatory and policy limitations